Introduction

There has never been a more important time to understand your UK tax position as a British expat.

The UK tax landscape is undergoing its biggest shift in over 25 years:

- Income from assets will be taxed 2% higher

- The non-dom regime is abolished from April 2025

- The UK is moving to a residence-based IHT system

- The 10-out-of-20 year rule decides global IHT exposure

- Class 2 NICs overseas are being removed

- Voluntary Class 3 NIC access is tightening

- Thresholds are frozen until 2031, pulling millions into higher tax bands

- SRT errors are rising sharply, especially for remote workers

- Residency rules now drive more of your taxation than your passport

- Double taxation is increasing, not decreasing

- HMRC enquiries into expats have risen sharply

More people are moving to the UK and more people are leaving - and most plan incorrectly

This guide gives you the full landscape - with no jargon, no fluff, no corporate wording.

Just clarity, strategy and lived experience.

Residency: The Core Of Everything

Residency is the heartbeat of UK tax.

It is the one test that decides:

- What you pay tax on

- Where you pay tax

- When you pay tax

- Whether your assets stay protected

- Whether your income is taxable

- Whether HMRC dictates the outcome or you stay in control

Most expats think residency is just about “where you live”.

In reality, it’s about day counts, ties, past years, future intentions, property availability, family connections, work patterns, and your economic footprint.

The Statutory Residence Test (SRT)

The SRT is the single most important tax test in your life if you:

- leave the UK

- remain abroad

- work across borders

- return to the UK

- spend part of the year in the UK

- own UK property

- have family in the UK

- invest in the UK

- run a business

The SRT decides your tax residency using a sequence of tests:

- Automatic Overseas Tests

- Automatic UK Tests

- Sufficient Ties Test

It applies in that order.

You stop at the first test that confirms your status.

Automatic Overseas Tests

You’re automatically non-resident if:

1. You spend <16 days in the UK (and you were UK resident in any of the previous 3 tax years).

2. You spend <46 days in the UK (and you were not resident in all of the previous 3 tax years).

3. You work full-time overseas AND

- spend <91 days in the UK

- AND

- work <31 UK workdays

A UK workday includes any day where you work for 3+ hours. Most expats can get caught on the third one because “workdays” are easy to misinterpret.

One Zoom call from London, replying to emails, signing documents? It can count.

Automatic UK Tests

You’re automatically UK resident if you:

- Spend ≥183 days in the UK

- Have a UK home available for ≥91 days

- Work full-time in the UK

Many returners accidentally trigger residency because they come back “gradually”, living between two countries.

The Sufficient Ties Test

If neither automatic test applies, your residency depends on how many UK ties you have and how many days you spend in the UK. Five UK ties matter:

- Family (partner/minor children in UK)

- Accommodation (available place to stay)

- Work (40+ UK workdays)

- 90-day tie (spend >90 days in the UK in either of the last two tax years)

- Country tie (you spend more days in the UK than any other country) – please note the country tie only applies to “Leavers” which is explained in further detail below.

Under the SRT, the Days × Ties rules are different depending on whether you are:

An Arriver (someone who was NOT UK-resident in any of the previous 3 tax years)

A Leaver (someone who was UK-resident in at least one of the previous 3 tax years)

Using the wrong one could trigger accidental residency, and so these concepts have been explained using the tables below:

A. ARRIVERS TABLE

(Not UK-resident in any of the previous 3 tax years)

{{INSET-IMAGE-1}}

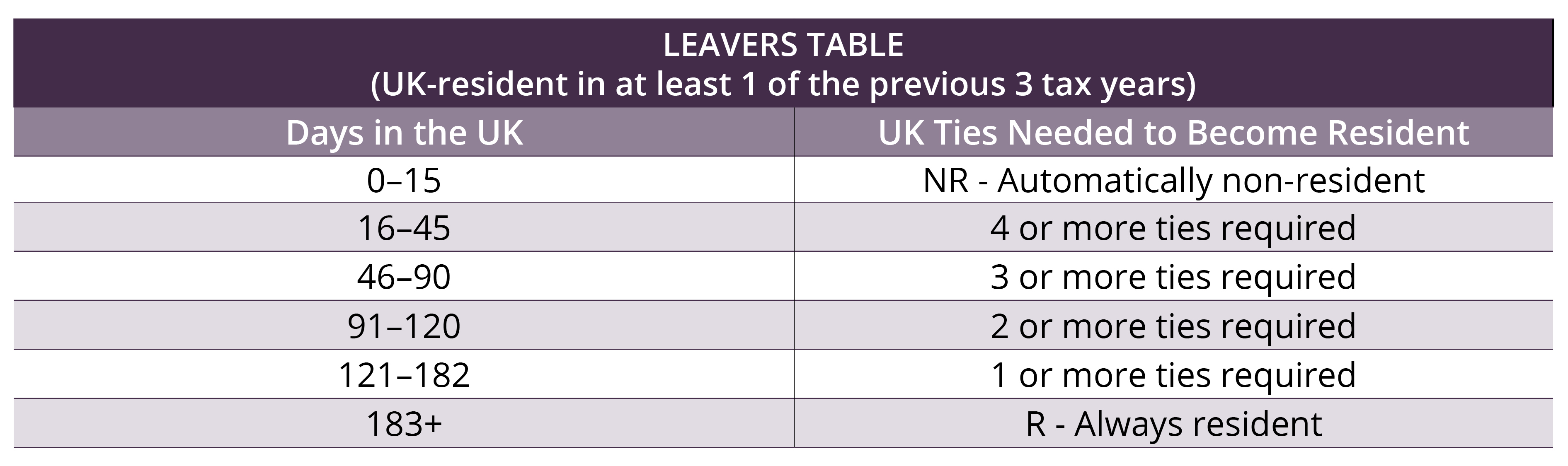

B. LEAVERS TABLE

(UK-resident in at least 1 of the previous 3 tax years)

{{INSET-IMAGE-2}} ** **

Comparing Arrivers and Leavers: The Day-Count Rules at a Glance

{{INSET-IMAGE-3}}

Why Expats Get It Wrong

Because most people assume: “I’ve been abroad for years - I’ll be treated as an Arriver.”

But if you were UK-resident even once in the previous three tax years, you are a Leaver - and the Leaver table is stricter.

This is where accidental residency can happen:

- dual-country living

- remote workers

- people returning “gradually”

- parents visiting children in the UK

- keeping a UK home

- UK workdays creeping into the year

- international executives flying in/out frequently

The SRT cares about patterns, not intentions.

In addition to the above, one detail many expats overlook is the 90-day tie. It looks back across a rolling two-tax-year window, so you can build this tie up gradually through holidays, work trips or family visits. Once you have it, the number of days you can spend in the UK before triggering residency can shrink unexpectedly in the following year and can cause your day-count threshold to do so, should you wish to maintain non-UK tax residence.

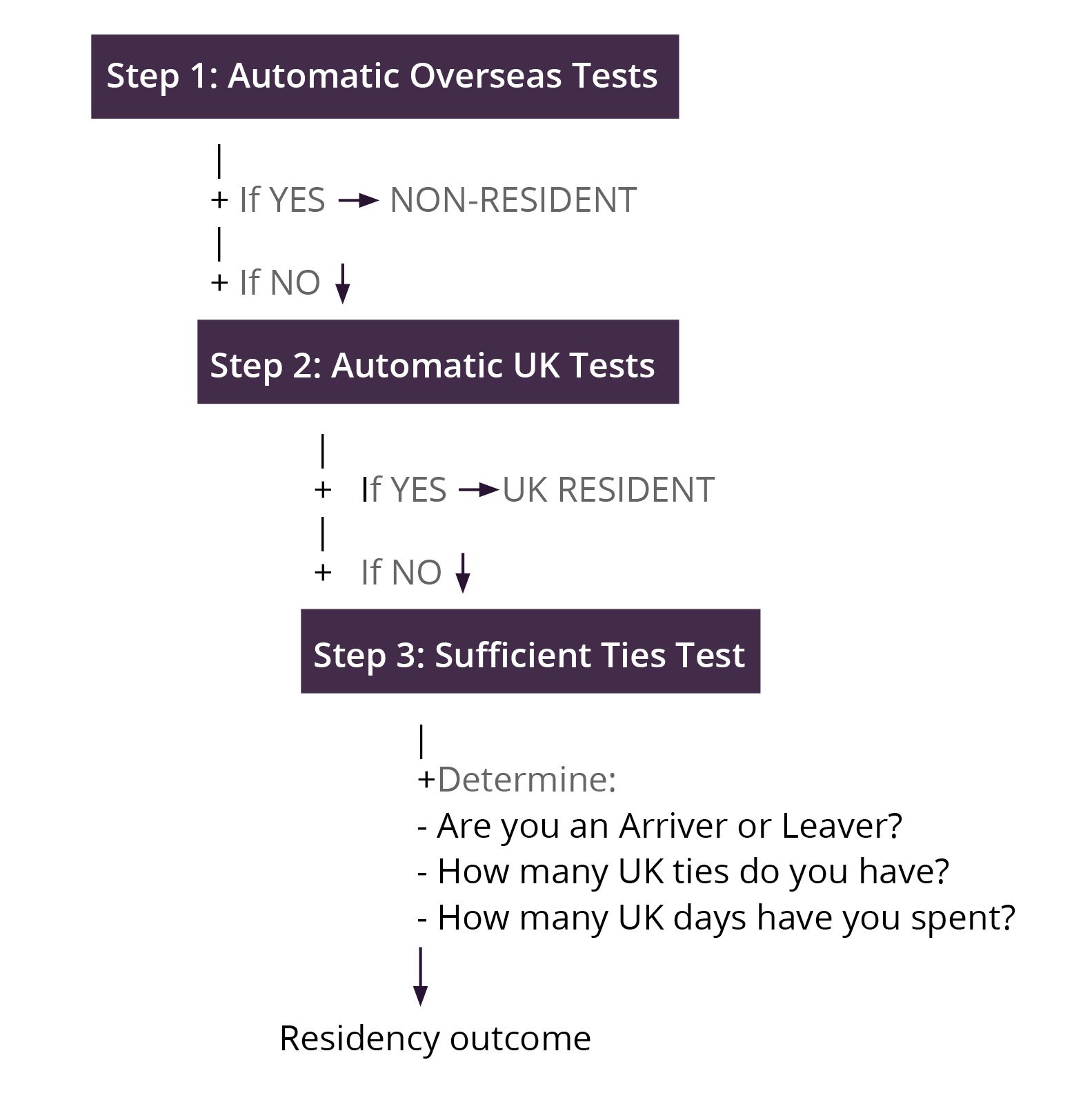

STATUTORY RESIDENCE TEST (SRT) flowchart:

{{INSET-IMAGE-4}}

Split years:

The SRT tells you whether you’re resident for the year as a whole. But there is a separate set of rules - the split-year provisions - that can divide the tax year into a UK part and an overseas part when you first leave or when you return. It’s a helpful relief, but only certain situations qualify, and many people assume it applies automatically when it doesn’t

Domicile: The Foundation Of Inheritance Tax

Residency decides your income tax.

Domicile previously decided your IHT, trusts, gifts, offshore assets and long-term wealth exposure. While residency can change every year, domicile was sticky. It followed your origin, your lifestyle, your emotional ties, your family and your long-term intentions. But from April 2025, the entire system changed.

The Old World (until April 2025)

Before April 2025:

- UK domiciled individuals were subject to UK IHT on their worldwide assets

- Non-UK domiciled individuals were subject to UK IHT only on their UK assets

- Long-term residents became “deemed domiciled” after 15 out of 20 years

- The remittance basis allowed non-doms to keep foreign income/gains outside UK tax

- Trusts created by non-doms could be “protected” and sit outside the UK estate

This framework created planning opportunities - but also huge complexity.

The New World (from April 2025)

The non-dom regime has been abolished and replaced with a residence-based system that is far more aligned with other OECD countries.

Here’s what now applies:

- Domicile no longer determines UK tax exposure for income and gains

- A residence-based system replaces the remittance basis

- UK IHT will also shift to a residence-based test, not domicile

- The key measure becomes 10 years of UK residence in the previous 20 years (“10/20 test”)

- When you leave, a “tail period” will continue your IHT exposure for a limited time

- Trusts will depend on settlor residence, not domicile, for their exposure

- Offshore income/gains cannot rely on remittance rules

This is one of the most significant tax reforms the UK has made in a generation - and it fundamentally changes how expats should plan.

Why this matters to expats

If you’re an expat - especially one returning to the UK - the shift to a residence-based IHT system changes the conversation entirely.

Under the new rules, your worldwide estate may become exposed to IHT if you:

- return to the UK and become resident again

- build up 10 years of UK residence within a 20-year window

- leave the UK but remain within the tail period

- hold assets in trusts where you are the settlor and you meet the residence test

This has three major implications:

1. Your IHT exposure may restart the moment you become resident

Even a short period of UK residence after years abroad may restart your 10-year clock.

2. Your exposure may continue even after you leave the UK

The tail period means your worldwide estate doesn’t switch off when you move overseas.

3. Your global assets - and your trusts - may need restructuring before returning

Because the new system ties exposure to residence, not domicile, long-term non-residents who believed they had “escaped domicile” may find themselves unexpectedly brought back into the UK IHT net.

If you previously believed:

“I lost my UK domicile years ago, so I’m outside the IHT system.”

That assumption is now outdated.

Under the 2025 reforms, domicile is no longer the shield it once was.

Your residence pattern - your day counts, your ties, your years of UK presence - becomes the deciding factor.

For many expats, this means rethinking:

- where assets are held

- how trusts are structured

- whether to return to the UK in a particular tax year

- how long to remain resident

- the sequencing of moves, gifts, distributions, and business exits

{{INSET-CTA-1}}

The New UK IHT System (2025–2026 And Beyond)

Inheritance Tax (IHT) remains the single biggest tax exposure for internationally mobile British families. It affects expats in the UAE, Asia, Europe - anywhere Brits build wealth and raise families. And from 2025 onwards, the rules that decide who is inside or outside the UK’s IHT net have changed more than at any time in the modern era.

Under the old regime, your domicile determined whether your worldwide estate was exposed to UK IHT. From 2025, that anchor is gone. The system is moving to a residence-based model, and what counts now is not where you were born, but how many years you spend as a UK resident over your lifetime.

Here’s what that means in practice:

The New IHT Framework (from April 2025)

1. Worldwide assets become taxable after 10 years of UK residence within a 20-year window

This is the new 10/20 test. If you’ve been UK-resident for a total of 10 tax years in the last 20, you fall within the scope of UK IHT - regardless of your historic domicile.

This means:

- A short return to the UK can restart your count.

- Long-term expats who return after many years abroad may enter the IHT net almost immediately.

- Families planning to repatriate need to understand exactly where they sit on the 10-year timeline before they relocate.

2. A “tail period” applies after leaving the UK

One of the most important features of the new regime is that IHT exposure does not end the day you become non-resident.

HMRC has confirmed that long-term UK residents remain within the IHT system for a residence tail after departure.

How long is the tail?

It depends on how many years you were UK resident:

- If you were resident for 10–13 years → tail = 3 tax years

- For each additional year of UK residence beyond 13 → add 1 year

- The tail is capped at 10 tax years

So an individual with 20 years of UK residence may remain exposed to UK IHT for up to 10 years after leaving.

This means:

- Moving abroad does not instantly disconnect your worldwide estate

- Planning must consider both residency history and future movement

- Returning briefly to the UK can change your exposure for a decade

For globally mobile families, the timing of moves becomes as important as the moves themselves.

3. Trusts now follow long-term residence, not domicile

Under the old regime, a non-dom could create a “protected” offshore trust: as long as they were non-UK domiciled when they settled the assets, non-UK property could sit outside UK IHT indefinitely.

From 6 April 2025, that changes. The key question is no longer “Were you non-dom when you set up the trust?” but:

“Are you a long-term UK resident (or within your IHT tail) when an IHT charge arises?”

If the settlor is a long-term UK resident at the time of a ten-year anniversary, an exit charge or their death, non-UK trust assets can be brought into the UK IHT net. If they are not long-term resident (and outside their tail), those assets can revert to excluded-property treatment.

This puts a spotlight on:

• long-standing offshore trusts settled by people who have built up 10+ UK resident years

• life assurance and wealth planning trusts created while UK resident

• trusts where future distributions or charges may arise after a return to the UK

For most internationally mobile families, that means trust reviews are now essential, not optional – especially where the settlor has a history of UK residence or is considering moving back**.**

4. Gifting strategies will need to be rewritten

The old domicile-based rules around:

- potentially exempt transfers (PETs)

- chargeable lifetime transfers (CLTs)

- excluded property

are all affected by the move to residence-based IHT.

For many expats:

- the timing of gifts,

- the choice of who holds assets,

- and the sequencing of movements in/out of the UK

will need to be rethought.

5. Spouse exemption may evolve under the new alignment

Historically:

- UK-domiciled spouse = unlimited exemption

- Non-UK domiciled spouse = capped exemption (£325k)

The reforms aim to modernise and align reliefs with the new residence-based approach. That may mean:

- increased reliefs for globally mobile couples,

- or more restrictions for mixed-residency families.

Either way: cross-border couples must reassess their estate planning.

The Human Reality Behind the New Rules

IHT isn’t just a tax.

It’s a tax on:

- your life choices,

- your time abroad,

- your return home,

- the way you provide for your family,

- and the story your estate tells when you’re gone.

Most expats don’t think about IHT until they have to - and by that time, the structure of their wealth, their residency history, and their timing decisions are already locked in.

The new regime raises the stakes.

Your exposure to IHT will now depend on decisions you may have made years ago, and decisions you’re about to make - like when to return to the UK, when to leave again, where to hold assets, and how trusts are structured. And the truth is simple:

Early planning gives you options. Late planning forces your hand.

Moving Abroad From The UK

Most expat tax problems begin before someone ever leaves the UK.

The 6–18 months before departure is the window where the biggest mistakes can happen.

Handled well, this period could reduce income tax, CGT and IHT exposure, and set up your new life abroad cleanly. Handled poorly, it can lock in avoidable tax charges for years.

The 18-Month Window - Why It Matters

The decisions you make in the run-up to leaving the UK can shape:

- your CGT position

- pension and share scheme taxation

- UK property exposure

- IHT under the new 10/20 rules

- how foreign income is treated once abroad

- whether Split Year Treatment applies

Small timing differences - even a month - can materially change the tax outcome.

Key Pre-Departure Actions

1. Review gains and losses

Crystallise gains or losses before leaving if it benefits your future tax position.

2. Review UK property

Understand CGT, NRCGT and how rental income will be taxed once non-resident.

3. Review share plans and business interests

Equity, options and bonuses often trigger charges based on where you are resident at key dates.

4. Restructure investments

Some UK funds are inefficient for non-residents; offshore structures may be more appropriate.

5. Review pensions

Consider contributions, consolidation and how income will be taxed overseas.

6. Organise bank accounts and offshore funds

Mixed or uncleansed funds can cause issues later.

7. Plan your NI position

With Class 2 removed and Class 3 tightening, make sure you understand your state pension record.

8. Establish a clear overseas pattern

HMRC expects evidence that your move is genuine - employment, accommodation, ties and timing all matter.

Split Year Treatment (SYT) - Helpful, but Easy to Lose

Many people assume SYT automatically applies. It doesn’t.

You can lose split-year treatment if:

- your overseas employment stops

- you return sooner than planned

- your UK home remains “available”

- your UK work activity exceeds the limits

- your UK days increase beyond thresholds

If SYT fails, your entire tax year may become UK-resident, meaning foreign income earned after departure can still be taxed in the UK.

The message is simple:

Plan your departure deliberately - don’t rely on assumptions.

Summary

Leaving the UK is a tax event, not just a relocation.

The 18-month window before departure gives you the opportunity to:

- restructure assets

- avoid accidental residency

- protect gains

- improve pension outcomes

- reduce long-term IHT exposure

Miss the window, and you lose control of outcomes you could have influenced.

Living Abroad As A UK Expat

For many people, the moment they land overseas, they relax.

“I’m abroad now - the UK can’t tax me.”

This is where most expats get caught out.

Living abroad does not mean you’ve left the UK tax system behind.

Certain income streams remain taxable. Certain reporting obligations remain. And choices you make while abroad can affect your future tax position when you return.

Below are the areas where expats most often misunderstand their exposure - and where early clarity prevents expensive surprises later.

1. UK Property - Still Taxable, Even When You’re Abroad

Owning UK property creates an ongoing UK tax footprint:

- Rental income remains taxable in the UK, even if you’re fully non-resident

- You may still need to file annual returns under the Non-Resident Landlord Scheme

- Mortgage interest relief changed and is more restricted

- NRCGT continues to apply on residential property disposals

- CGT applies on UK residential property gains - non-residents are not exempt

- SDLT surcharges can apply when non-residents buy UK property

Property is the most common reason non-residents continue interacting with HMRC - sometimes without realising they should be.

2. UK Investments - Some Income Remains Taxable

Being non-resident doesn’t automatically remove UK tax on all investments.

Depending on what you hold, you may still have UK exposure on:

- UK shares

- UK funds and OEICs

- UK ETFs

- ISAs (you cannot keep contributing once non-resident)

- UK corporate bonds

- UK dividends

Even when gains are non-UK taxable, income may still be.

And many UK funds are deeply inefficient for expats once they leave the UK.

The solution is simple:

Review your portfolio the moment you become non-resident.

3. Pensions - The Rules Abroad Are Different

The taxation of UK pensions overseas depends heavily on:

- your country of residence

- the Double Tax Treaty (DTA)

- how you take income (lump sum vs. drawdown)

- whether you are taking your Pension Commencement Lump Sum (PCLS)

- local withholding taxes

- your future UK re-entry plans

- the currency you receive income in

Many expats assume pensions are simple.

In reality, they are one of the most complex cross-border tax areas - especially when planning withdrawals before or after returning to the UK.

4. State Pension - The Rules Have Tightened

From 2026 onwards:

- Class 2 NIC for expats is abolished

- Class 3 contributions will become harder to qualify for

- You now need 10 qualifying years for any state pension

- Years abroad do not automatically count

- Frozen thresholds mean expats must plan more deliberately

Failing to plan NIC contributions early can leave a permanent gap in your retirement income.

5. Bank Accounts - Mixed Funds Are a Serious Issue

Under the new regime, “mixed funds” - accounts that contain a blend of income, gains and capital - can create long-term tax and remittance complications.

If you don’t organise and “cleanse” your funds before leaving the UK, you may find:

- withdrawals become hard to trace

- foreign income becomes inadvertently taxable

- returning to the UK creates unexpected issues

A clean banking structure makes life abroad far simpler.

6. Capital Gains - Timing Still Matters When You Live Abroad

Most CGT planning happens before you leave or after you return, but events during expat life can still matter.

Common issues include:

- the UK’s rules on UK land and property

- share disposals relating to UK employment

- gains tied to UK situs assets

- planning for a future return

- managing residency for CGT purposes

Just because you are non-resident does not mean you are outside the reach of UK CGT rules in every situation.

Summary

Living abroad offers opportunity - but not immunity.

The UK tax system still applies to:

- property

- certain investments

- pensions

- NIC

- specific capital gains

- bank account structures

The expats who thrive are the ones who stay informed, stay organised, and plan not just for life abroad - but for the possibility of returning someday.

Returning To The UK

The UK tax system resets the moment you become resident again. Income, gains, pensions, trusts, funds, property, and cash movements all get reassessed under UK rules. That’s why expats returning without preparation often face unexpected charges, enquiries, or lost planning opportunities.

Here are the issues that catch people most often.

Most common mistakes

- Believing foreign income remains “foreign” once resident - it doesn’t. Once you’re UK resident, the worldwide arising basis applies unless a specific exemption or treaty rule says otherwise.

- Assuming the UK tax year follows calendar years - arriving in March vs April can change your tax exposure by an entire year.

- Not planning the timing of arrival - one poorly chosen return date can pull foreign salary, bonuses, gains or distributions into UK taxation.

- Bringing money back to the UK without cleansing it - mixed funds are one of the most common causes of accidental taxable remittances.

- Returning with mixed or opaque offshore accounts - without proper categorisation, withdrawals may become taxable even when the underlying funds are not.

- Returning with appreciated assets - gains made while non-resident may be caught if you dispose after becoming UK resident again.

- Returning with unreported foreign income - HMRC receives automatic data through CRS; undeclared income often surfaces within months of returning.

- Receiving trust distributions before returning - certain payments can create tax exposure once UK residence restarts.

- Coming back without a pension strategy - the taxation of drawdowns, lump sums and overseas pensions can change overnight on re-entry.

- Arriving in the wrong month - a difference of days can determine whether split-year treatment applies, and whether an entire year of foreign income is pulled into UK tax.

The most expensive mistake

Believing you can “fix everything once you’re back.” You can’t.

By the time your return flight touches down, most of the meaningful planning opportunities have already passed. The UK tax system looks at facts, timing and residence status - not explanations or intentions. A well-timed return can protect income, preserve gains, ring-fence funds and avoid unnecessary exposure. A poorly timed return can create tax issues that take years to unwind. Planning ahead is not optional - it’s the most valuable part of the repatriation process.

{{INSET-CTA-2}}

How DTAs Protect (Or Fail To Protect) Expats

Double Tax Treaties (DTAs) are often misunderstood. Most expats think a treaty “moves” taxation to the more favourable country. It doesn’t. A DTA simply tells each country who gets to tax what, and how to prevent the same income being taxed twice.

DTAs matter for almost every type of cross-border income:

- salary and employment income

- dividends and portfolio income

- rental income

- business profits and self-employment

- director fees

- pensions and annuities

- gains on certain assets

- property-related income

Used correctly, a DTA gives clarity and prevents overlapping tax bills. Used incorrectly, it leads to overpayments, incorrect filings, penalties, or unexpected UK tax when you return.

What DTAs do not do is transfer tax advantages from one country to another.

A person living in a zero-tax jurisdiction can still face UK tax on UK-source income, even if a treaty exists.

This is where many expats get caught out - especially on pensions.

A British expat may receive overseas pension income tax-free while abroad, but when they return to the UK, the DTA no longer protects them. The income becomes fully taxable under UK rules unless the treaty explicitly says otherwise. In most cases, it doesn’t.

DTAs prevent double taxation.

They do not eliminate UK taxation once you’re resident again - and they do not override the Statutory Residence Test.

For expats, DTAs are a safety net, not a strategy.

Understanding what they cover - and what they don’t - is essential before leaving the UK, while living abroad, and especially before returning.

Investing As An Expat

When you become an expat, the rules around investing shift. Many people focus on where their money is invested - UK, offshore, local markets - but that’s not the determining factor of how their income and gains are taxed.

The real driver is your tax residence, not the investment’s postcode.

Where you live matters more than where your money lives.

Once you understand that, the rest becomes far clearer.

Different structures behave very differently depending on your country of residence, your future plans, and whether you intend to return to the UK.

Investment structures that may work well for expats

These can offer tax deferral, cleaner reporting, wider access to funds, and flexibility across jurisdictions:

- international portfolio bonds

- offshore collective investment structures

- globally distributed funds

- retirement wrappers suited to expatriates

- certain company structures (when used correctly and with substance)

- trusts (now more complex post-2025, and more dependent on residence rules)

Used properly, these structures can reduce friction, simplify reporting and give you more control over how income and gains surface for tax purposes.

Investment structures that may cause problems

These often remain tax-inefficient, inflexible, or complicated once you leave the UK:

- UK unit trusts

- UK OEICs

- ISAs (you cannot contribute while non-resident, and they may lose local tax advantages)

- holding UK shares in personal form, rather than through an appropriate wrapper

The common theme: investments that are efficient for UK residents are not always efficient for non-residents. Your investment structure should match your residency, your trajectory, and your intended return - not just your risk tolerance.

For expats, the right structure does far more than grow your money.

It controls how accessible it is, how it’s taxed, and how it fits into your long-term global plan.

The New 2% Tax Uplift & What It Means For Expats

From April 2026–2027 the UK government has raised tax rates on certain types of passive income - a change that affects many expats who rely on dividends, savings, rental income or portfolio cash flows.

What’s changed

- From 6 April 2026, dividend tax rates rise by 2 percentage points: basic-rate dividend tax goes to 10.75%, higher-rate dividend tax to 35.75%.

- From 6 April 2027, savings interest and property (rental) income will also be taxed at rates 2 percentage points higher than before.

Who is most exposed

If you are living abroad - or planning to - these changes matter if you rely on:

- dividend income from UK or international holdings

- savings interest or yields

- rental income from UK (or property income taxed in UK)

- portfolio income and distributions from funds or trusts

Even for non-residents, UK-source income remains subject to relevant UK tax rules, and higher rates mean lower after-tax yields.

What this means when you return (or if you keep UK income while abroad)

- Returning to the UK with dividend/pension/portfolio income - now at higher rates - means you must carefully recalculate after-tax cash flows.

- Passive income becomes more expensive - planning must adapt.

- For globally mobile professionals, this may shift the balance: tax-efficient wrappers, offshore structures, timing of returns, and residency strategy become more important.

What this does not do

Tax increases of 2% do not magically bring all asset income into the same tax bucket.

- They apply only to dividends, savings interest, and property (where relevant).

- They do not convert pension income, employment income, or capital gains.

- They do not override tax treaties or residency-based exemptions.

In other words - the uplift makes passive income more costly, but does not change the underlying rules about what is taxable.

Bottom line for expats

Expect lower net returns on dividends, savings, and rental income from 2026 onward.

If you thought your passive income streams were stable, they aren’t any more.

If you live abroad or plan to return, re-run your numbers.

If you rely on passive income, consider restructuring - wrappers, offshore funds, timing, residency.

Taxable yield is increasing, and advice will now matter more than ever.

National Insurance Changes For Expats

The National Insurance landscape is undergoing one of the biggest shifts in decades - and for expats, it changes the way you build and protect your UK State Pension.

Many people living abroad assume they can “catch up later.” Under the new rules, that assumption is no longer safe.

Class 2 contributions abolished overseas

For years, Class 2 NIC allowed expats to build pension entitlement at a low cost. This option is now being removed, closing a route that thousands relied on.

Class 3 eligibility tightened

Class 3 contributions remain available but will be harder to access. The UK wants clearer evidence of previous connection and entitlement, making “topping up” far less flexible than before.

10-year minimum still applies

You need at least 10 qualifying years for any State Pension, and 35 years for a full one. With overseas years no longer counting as easily, many expats will fall short without deliberate planning.

Years abroad no longer automatically top-up eligible

Previously, people working abroad could often buy missing years with limited friction. That era is ending. The rules now require more checks, more evidence, and stricter qualifying criteria.

Most expats will fall short unless they plan early

Between the removal of Class 2 and the tightening of Class 3, the UK is making it harder for expats to accumulate pension years while overseas. Gaps can now persist for life if not addressed in real time.

This will become one of the most expensive - and most avoidable - expat mistakes of the next decade.

Planning your NIC position early ensures you don’t lose part of your retirement income simply because the rules changed while you were abroad.

Case Studies

Sometimes the clearest lessons come from real people who made real mistakes.

These examples show how quickly things can go wrong - and how easily they could have been avoided with the right planning.

Case Study 1 - The Accidental Returner

A British expat moves back to the UK in February, assuming their foreign salary remains “foreign.”

But because of the UK tax year running to 5 April - and because they failed to secure Split Year Treatment - they become UK resident for the whole year.

The result:

Their overseas income for the full tax year becomes taxable in the UK. All avoidable with correct arrival timing and SRT planning.

Case Study 2 - The Investor in Dubai

A long-term Dubai resident relies on dividends to fund their lifestyle.

They return to the UK in 2026, unaware of the new, higher dividend tax rates.

Their portfolio generates £580,000 of dividends a year. The 2 percentage point uplift alone adds:

£11,600 in additional annual UK tax.

And because they are now UK resident, their entire dividend income is taxed - something that wasn’t even on their radar before returning.

Case Study 3 - The Family With a UK Property

A family living in Hong Kong assumed that being non-resident meant no UK tax on selling their old UK home. They were wrong. Non-residents are still fully within the scope of NRCGT on UK residential property.

The gain on sale resulted in an unexpected CGT bill.

Case Study 4 - The Non-Dom Who Thought They Were Safe

A non-UK domiciled executive lived abroad for 15 years, believing she had “left UK IHT behind forever.” She returns in 2026.

Under the new residence-based IHT rules, her worldwide assets fall back into UK IHT exposure as soon as she becomes UK resident - because she meets the 10 out of 20 years threshold from earlier in her career.

Her global estate is now within the UK IHT net.

A problem she thought she escaped decades ago.

Common Expat Tax Mistakes

Most expat tax problems aren’t caused by complexity. They’re caused by assumptions.

Below are the mistakes that surface again and again - the ones that cost expats the most time, money and stress.

Misunderstanding the Statutory Residence Test (SRT)

People rely on intuition instead of the rules. SRT is mechanical - ignore it, and you may drift into UK residence without realising.

Returning in the wrong month

A return in March instead of April can drag an entire year of foreign income into UK taxation.

Holding UK funds while non-resident

UK OEICs and unit trusts often become inefficient once you live abroad.

Not cleansing offshore accounts

Mixed funds create years of unnecessary complexity - and unexpected UK tax on return.

Accidentally triggering the worldwide arising basis

One step back into UK residence, even briefly, can bring your entire global income into UK scope.

Assuming a Double Tax Treaty protects everything

DTAs prevent double taxation, not UK taxation. Many sources of income remain taxable on return.

Forgetting UK property reporting obligations

Non-resident does not mean “non-reporting” - CGT, rental income and NRCGT still apply.

Thinking pensions are always tax-free overseas

Different countries apply different rules; DTAs vary. Returning to the UK changes everything overnight.

Believing “I’m offshore so HMRC can’t tax me”

UK-source income remains taxable. CRS reporting means HMRC already sees the data.

Not planning National Insurance

The removal of Class 2 and tightening of Class 3 mean expats can fall short of their State Pension without realising.

Not documenting domicile or long-term residence status

Under the new 10/20 rules, unclear records lead to unexpected IHT exposure.

Marrying a UK-domiciled spouse without planning

Spouse exemption rules are changing - and can significantly increase IHT risk in cross-border families.

Letting share schemes vest at the wrong time

Share vesting while UK-resident - or becoming UK-resident shortly afterwards - can trigger avoidable income tax bills.

Practical Step-By-Step Guide

A globally mobile tax position only works when your actions match your intention.

Whether you are leaving the UK, living abroad, or returning home, these are the practical steps that protect you.

If you’re leaving the UK

- Confirm your SRT position and break UK residence cleanly

- Understand which SRT case applies and whether you need to reduce ties before the departure date.

- Secure Split Year Treatment (SYT)

- Make sure your move satisfies the relevant SYT case. Once lost, SYT cannot be “fixed” later.

- Review your investments

- Switch out of UK-inefficient structures and into expat-appropriate wrappers where needed.

- Review UK property

- Assess rental income, CGT exposure, NRCGT, and whether ownership still makes sense as a non-resident.

- Organise pensions

- Consider contributions, consolidation, overseas taxation and timing of future withdrawals.

- Cleanse and structure bank accounts

- Avoid mixed funds before they become long-term reporting and remittance problems.

- Document your residence history for future IHT and trust rules

- Post-2025, your residence record is more important than your domicile narrative.

- Plan your National Insurance position

- With Class 2 abolished and Class 3 restricted, understand how your state pension will be protected.

If you’re living abroad

- Track UK day counts

- Most accidental residents never realise how close they are to triggering SRT.

- Track UK ties

- Family, accommodation, work and past presence all matter - and ties can appear earlier than people expect.

- File UK property tax correctly

- Rental income and disposals remain UK-taxable. Reporting obligations don’t disappear.

- Manage your UK investments

- Check whether UK funds, OEICs or direct shareholdings are still appropriate for a non-resident.

- Manage pensions proactively

- Understand how your DTA works, how withdrawals are taxed locally, and plan for future UK re-entry.

- Review your IHT exposure under the 10/20 residence rule

- Long-term residence or frequent returns can unexpectedly bring worldwide assets into scope.

- Review your transitional position if you previously relied on non-dom rules

- Existing trusts, gifting strategies and excluded property structures may need updating.

If you’re returning to the UK

- Choose your arrival month deliberately

- A difference of days can determine whether a full year of foreign income becomes taxable.

- Cleanse funds before arriving

- Once you are UK-resident, mixed funds become far harder to unwind.

- Review foreign income streams

- Salary, business profits, dividends, pensions or trust distributions may all become taxable on arrival.

- Review pensions

- Returning can change how withdrawals, lump sums and overseas pensions are taxed.

- Plan disposal timing

- Gains realised after becoming UK-resident may fall fully into UK CGT.

- Document your UK residence date

- HMRC will rely on facts, not your intentions. Keep clean evidence.

- Rebuild your National Insurance record

- Understand which gaps remain and whether Class 3 contributions are still available.

- Align your currency position

- Exchange rates can materially affect taxable gains, remittances and investment outcomes.

Future Changes & Risk Factors

The UK tax system is moving toward greater transparency, higher taxation of passive income, and tighter alignment with international standards. For expats, this means the landscape will continue to shift long after 2026.

Here are the risk factors shaping the next decade of cross-border tax:

Rising UK tax load on asset income

Dividend, savings and property income rates are increasing - and more adjustments are likely as the UK broadens its revenue base.

A more assertive HMRC

HMRC now receives real-time data from overseas banks and tax authorities. Enquiries into expats and returners have risen sharply, especially where residence, offshore income or mixed funds are involved.

Alignment with OECD frameworks

The UK continues adapting to global anti-avoidance standards. Expect closer alignment with OECD rules on cross-border income, transparency, and the treatment of offshore structures.

Increased scrutiny of expat income

Salary, business profits, director fees, pensions and trust distributions are now more closely examined, particularly when expats move in and out of UK residence.

NI reforms designed to raise revenue

With Class 2 abolished and Class 3 restricted, the State Pension system is tightening. Expats will need more deliberate planning to avoid permanent gaps.

IHT likely to tighten further

The move to a residence-based regime is only the first step. The government will almost certainly refine the 10/20 rules, the tail period and trust treatment over time.

Potential CGT reforms

CGT is politically attractive to adjust and remains under periodic review. Expats with appreciated assets should expect future changes.

Remote work rules tightening

Cross-border remote working creates dual-tax exposure. Expect stricter guidance on where work is “performed” for tax purposes.

Greater banking transparency (CRS)

CRS data-sharing expands every year. HMRC increasingly receives detailed information on overseas accounts, investments and income - often before the taxpayer files.

The direction of travel is clear:

more transparency, more alignment, more scrutiny - and more importance placed on getting residency right.

Conclusion

Being a British expat is rewarding, liberating and full of opportunity.

But the tax system follows you - wherever you go.

In 2026, the rules are harsher. The traps are deeper. The consequences are bigger. And the planning window is shorter.

But with the right strategy - and the right adviser - every one of these risks can be managed, avoided or turned into an opportunity.

The key is simple:

Don’t wait until HMRC forces the issue.

Act while you still control the outcome.