Spanish Tax

10 Questions You Should Ask About Finance and Tax When Moving from the UK to Spain

Planning a move to Spain? Kelman Chambers outlines the key tax and finance questions UK residents must answer before relocating.

December 14, 2025

This is a div block with a Webflow interaction that will be triggered when the heading is in the view.

If you’re living in Spain or planning to move there, understanding how your assets will be taxed is essential, and increasingly urgent. Spain’s Wealth Tax and Solidarity Tax on Large Fortunes have become two of the most significant issues facing high-net-worth individuals (HNWIs) and international residents.

These taxes are complex, heavily influenced by regional politics, and evolving quickly, but the consequences for getting it wrong can be severe.

This updated 2025 guide breaks down what you need to know, how the rules vary, and the most effective planning strategies available.

Spain’s Wealth Tax (Impuesto sobre el Patrimonio) is an annual tax levied on the net value of your personal assets as at 31 December each year.

Spain’s Wealth Tax applies to a broad range of personal assets, including real estate both within Spain and abroad, bank accounts, investment portfolios, boats, cars, art, and jewellery. Life assurance bonds may also be included, depending on their structure, as well as shareholdings in private and listed companies. Pensions in drawdown may be taxable in some cases. All assets are assessed at their fair market value as of 31 December each year, and liabilities, such as mortgages and loans, can be deducted from the total asset value.

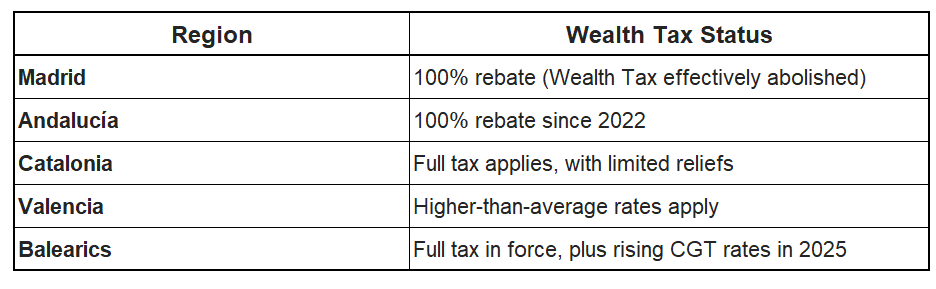

Each individual receives a €700,000 personal allowance, plus an additional €300,000 exemption for their main home in Spain (if resident). That gives most residents up to €1 million in exempt wealth. But here’s the catch: Wealth Tax is devolved to Spain’s 17 autonomous regions, and treatment varies dramatically.

Regional Examples (2025):

You must pay according to the region where your primary residence is located (as determined by the highest number of days spent).

In December 2022, Spain introduced the Impuesto Temporal de Solidaridad de las Grandes Fortunas (Solidarity Tax on Large Fortunes), originally a “temporary” two-year measure but now extended into 2025 and widely expected to remain in place.

The Solidarity Tax was introduced to standardise taxation across Spain and close loopholes created by regional Wealth Tax reductions. This measure overrides local exemptions, ensuring that high-net-worth individuals in wealthy regions, where Wealth Tax was abolished, still contribute their fair share.

The tax allows for a €700,000 exemption per person, the same as the Wealth Tax. In addition, there is a €300,000 exemption for your main residence, which is applied on top of the €700,000 personal allowance. The Solidarity Tax applies to net wealth exceeding €3 million, with rates as follows:

It’s important to note that if you’ve paid Wealth Tax in your region, that payment is credited against the Solidarity Tax. However, if you live in a region like Madrid, where Wealth Tax is abolished, you will be liable for the full Solidarity Tax without any rebate.

The 60/20 Rule is a lesser-known provision that can help limit your total Wealth and Solidarity Tax liability. Under this rule, your combined tax on income (IRPF) and Wealth/Solidarity Tax cannot exceed 60% of your taxable income. However, the tax cannot be reduced below 20% of the original amount.

For example, if you have €5 million in net assets and earn €200,000 in income, your total Wealth/Solidarity Tax combined with income tax cannot exceed €120,000. If the calculated tax exceeds this limit, you may apply for a reduction, but you’ll still be required to pay at least 20% of the original Wealth/Solidarity Tax amount.

It’s important to remember that this relief is not automatic; you must request it on your tax return. Additionally, not all asset types or structures easily qualify for this reduction.

If you’ve moved to Spain in 2024 and are tax resident by 31 December, your global assets as of that date are assessable.

If your net worth exceeds €3 million and you live (or plan to live) in Spain, this is a non-negotiable area for planning.

Use International Investment Structures - Investment platforms based in Ireland, Luxembourg, or Malta can provide several benefits, including the deferral of tax on income and gains, lower reporting obligations, and potential protection from Wealth and Solidarity Tax, depending on the investment structure. Additionally, some bonds that comply with Spanish regulations may be excluded from Wealth Tax calculations if they are structured correctly.

Leverage Debt Strategically - If you hold Spanish real estate, consider mortgaging or refinancing. Secured liabilities reduce net asset values, reducing taxable wealth.

Rebalance Asset Types - Shifting wealth from taxed categories (e.g. shares, property) to non-taxable or lower-tax structures can reduce your exposure without reducing lifestyle.

Plan Residency Dates Carefully - Moving after 1 July may allow you to delay tax residency to the following year, preserving a tax-free planning window for global restructuring.

Every year, thousands of Spanish tax residents find out from their accountants in June that their Wealth or Solidarity Tax bill is significantly higher than expected.

The reality is: your 2025 tax bill was decided on 31 December 2024. That date has already passed. If you didn’t plan ahead, if your portfolio wasn’t structured, your assets weren’t reviewed, or your residency status wasn’t managed, then options are limited.

But the good news? You still have time to prepare for next year.

Whether you’re already living in Spain or planning a move, we help HNW individuals optimise their global structures and avoid unnecessary exposure to Spanish wealth taxes.

Andy is a highly experienced financial services professional and joined Skybound Wealth Management from a major European Wealth Management business, bringing with him considerable industry knowledge and expertise.

This material is for general informational purposes only and does not constitute personalised financial, tax, or legal advice. Rules and outcomes vary by jurisdiction and individual circumstances. Past performance does not predict future results. Skybound Insurance Brokers Ltd, Sucursal en España is registered with the Dirección General de Seguros y Fondos de Pensiones (DGSFP) under CNAE 6622 , with its registered address at Alfonso XII Street No. 14, Portal A, First Floor, 29640 Fuengirola, Málaga, Spain and operates as a branch of Skybound Insurance Brokers Ltd, which is authorised and regulated by the Insurance Companies Control Service of Cyprus (ICCS) (Licence No. 6940).

Ordered list

Unordered list

Ordered list

Unordered list