Spanish Tax

10 Questions You Should Ask About Finance and Tax When Moving from the UK to Spain

Planning a move to Spain? Kelman Chambers outlines the key tax and finance questions UK residents must answer before relocating.

December 14, 2025

This is a div block with a Webflow interaction that will be triggered when the heading is in the view.

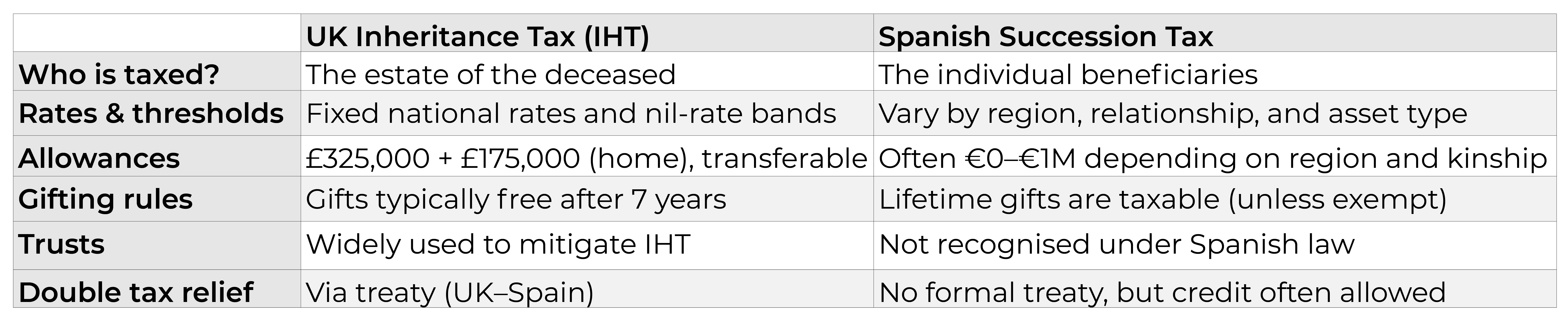

If you’ve relocated to Spain or are planning to, understanding Succession and Gift Tax (Impuesto sobre Sucesiones y Donaciones) is essential. Unlike the UK’s inheritance tax system, which focuses on the deceased’s estate, Spain operates under a very different approach, and this can have significant financial implications for both you and your heirs.

This article explores the key differences between the Spanish and UK systems, outlines planning strategies, and provides the most important updates you need to know. Whether you’re a British expat, a foreign investor with Spanish assets, or building a global estate, understanding these nuances is crucial in 2025 and beyond.

Spain's system of succession tax is highly decentralised, with each of the country’s 17 autonomous communities setting its own rules, reliefs, and allowances. As a result, the gap between the best and worst regions is significant, which can dramatically impact the tax burden. Beneficiaries are classified into four categories: Group I includes children under 21, Group II includes children over 21, parents, and spouses, Group III includes siblings, aunts/uncles, nieces/nephews, in-laws, and stepchildren, while Group IV covers distant relatives and non-relatives. The treatment of stepchildren, however, remains ambiguous in some regions and may fall under either Group III or Group IV depending on the circumstances and location.

For example, in key regions in 2025, Andalucía offers a €1 million exemption per heir along with a 99% tax reduction for Groups I and II. Madrid offers a 99% tax reduction for close relatives, while Catalonia provides smaller exemptions, progressive rates, and fewer discounts.

In Spain, the tax burden follows the beneficiary, not the estate. If the beneficiary is a Spanish tax resident, they are taxed on everything they inherit, including worldwide assets. However, if the beneficiary is not a Spanish tax resident, they are only taxed on Spanish assets, such as property and bank accounts. For example, if a Spanish resident passes away leaving €1.5 million in global assets, their child who lives in the UK would only pay tax on the Spanish assets. In contrast, their child living in Spain would pay tax on the entire inheritance, including the global assets.

Until recently, UK inheritance tax (IHT) was based on domicile, a vague and often difficult-to-define concept. However, from April 6, 2025, HMRC introduced a clearer test. If someone has been a UK tax resident for 10 of the previous 20 years, their worldwide assets will remain subject to UK IHT. If they haven’t met this criterion, only their UK assets will be taxed.

These changes make it even more crucial for expats to carefully track their years of UK residency, plan asset locations with tax efficiency in mind, and consider the succession implications in both the UK and their country of residence.

UK advisers often recommend trusts to mitigate inheritance tax. But Spain doesn’t recognise trusts as legal entities, meaning:

If you’re resident in Spain or your heirs are, avoid relying on trusts as your primary succession strategy.

As of 2025, UK pensions are considered part of your inheritance tax (IHT) estate, which means that even if your pension is left outside your will, it could face a 40% tax charge upon your death. Spain may also seek to tax pension assets under certain conditions, particularly if the pension has been drawn down. Additionally, the Overseas Transfer Charge (OTC) now applies if you transfer your pension to a country where you are not a resident, resulting in a 25% tax charge.

In some situations, it may be more beneficial to accept the 25% tax hit now, rather than leaving your heirs with the prospect of a 40% tax charge on a larger amount in the future.

Minimise Spanish Assets

It is advisable to avoid holding excessive wealth in Spanish real estate or bank accounts if your heirs are not Spanish residents. Instead, consider moving your wealth into international investment wrappers located in countries such as Ireland, Luxembourg, or Malta. These are EU-regulated, but not classified as Spanish situs assets, meaning they are less likely to be taxed under Spanish succession laws.

Use a Usufruct Structure

A usufruct structure is a Spanish legal concept that allows a spouse to live in a property rent-free while the children inherit the title. This is similar to a life interest trust, and it helps reduce the taxable value transferred to heirs, offering a strategy for mitigating succession tax.

Avoid UK Asset Bloat

If you are no longer a UK inheritance tax (IHT) resident, it is important to avoid accumulating unnecessary UK-based wealth. This is especially significant now that pensions are fully assessable for IHT, which can increase the tax burden on your estate.

Track Your Status in Both Countries

Your UK residency impacts your IHT liability, while your Spanish residency will determine your exposure to succession tax. Additionally, the residency status of your heirs will influence what they will need to pay in Spain, so keeping track of this information is crucial for effective planning.

Consider International Portfolios

Modern investment accounts held through EU platforms offer significant advantages, including growth potential, income tax deferral, and succession planning benefits. Furthermore, these investment accounts are compatible with Spanish law, making them a valuable tool for cross-border wealth management.

No. There is no formal double tax treaty for inheritance or succession tax.

However, Spain will generally offer a unilateral credit for tax already paid in the UK. However, if UK tax is higher than Spain, no refund is given. And If Spain calculates a higher bill, you may have to pay the difference.

Between October 2024 and April 2025, the UK introduced three major changes to inheritance tax and pension rules. As governments look to increase tax revenue, more changes are likely, in both Spain and the UK. That means ongoing reviews are no longer optional. They’re essential.

Most families don’t plan to leave a tax bill behind. But without cross-border succession planning, that’s exactly what happens.

Tax planning isn’t just about mitigation. It’s about ensuring your wealth ends up where you want it, with the people you love, without unnecessary erosion along the way.

Want to explore your options? Our international tax and estate planning team specialises in helping UK expats and Spanish residents structure their assets effectively.

Kelman holds the prestigious Level 6 Chartered Financial Planner qualification from the CII in the U.K. and the EFPA European Financial Planner qualification, demonstrating his commitment to the highest standards of professional expertise across both the U.K. and Europe.

Specialising in investments and tax & intergenerational wealth management, Kelman stays at the forefront of cross-border tax planning and wealth transfer strategies. His expertise ensures that clients are not only optimising their wealth today but also planning for future generations in the most tax-efficient way.

Ordered list

Unordered list

Ordered list

Unordered list