The Truth About SRT and the Rules That Actually Matter

Let’s be honest - most people think becoming “non-resident” is simple.

You move abroad. You get a new job. You book a one-way ticket. You settle into life overseas.

And you assume HMRC waves goodbye and switches you off.

But that’s not how it works.

The truth is this:

You can physically leave the UK and STILL be UK tax resident.

You can be living in Dubai, Singapore or Europe…

earning in a foreign currency…

paying tax elsewhere…

and yet HMRC still sees you as theirs.

Why?

Because residency in the UK isn’t emotional. It isn’t about your postcode. It isn’t about your intention. And it definitely isn’t about where you feel you live.

Residency is a rules-based test: technical, structured and evidence driven. And it can be difficult to navigate if you don’t understand the rules. I’ve seen people who genuinely believed they had left the UK - months, even years ago - discover they remained fully UK tax resident without realising it.

The cost?

In some cases, very significant. Income taxed globally. Foreign income captured. Worldwide gains exposed. Overseas pensions unintentionally taxable. IHT exposure potentially increasing.

HMRC enquiries triggered. Split-year denied. Double taxation complications.

And all because they didn’t understand a significant set of rules - rules that decide your entire tax reality. This article explains those rules, clearly, honestly, and in plain English.

Introduction

The Statutory Residence Test (SRT) is the backbone of UK expat taxation.

If you want to become non-resident:

- This is the test HMRC will use to determine your status.

- This is the test you need to satisfy.

- This is the test some expats fail without even realising.

Why?

Because SRT doesn’t always align with how people intuitively think about “where they live”. It applies set criteria, and small details can change the outcome.

You can live abroad for a large part of the tax year, but still remain UK resident depending on your UK days, ties and work pattern – for example if:

- your children live in the UK

- your spouse stays behind

- you kept a UK home

- you visited “too often”

- you came back for work

- your work pattern was non-compliant

- you created a tie without noticing

- you crossed a day-count threshold

- you didn’t document your move

- your travel pattern contradicted your story

And what happens if you accidentally remain UK resident?

You can become taxable on:

- your worldwide income

- your foreign employment

- your overseas property

- your investment income

- your offshore gains

- your pension income

- your business income

- your company distributions

This guide is designed to help you understand and reduce the risk of that outcome.

Why SRT Exists

Before 2013, UK residency was vague.

It relied on case law, intention and “ordinary residence”.

It was messy, subjective and open to interpretation.

So HMRC introduced SRT - a statutory framework designed to:

- reduce subjectivity

- increase certainty

- reduce disputes

- improve consistency in outcomes

SRT gives HMRC a clear framework.

If you meet the criteria - you’re resident.

In many cases, once the facts are clear, there is limited scope to rely on intention alone.

SRT leaves little room for interpretation. It tends to work best when your position is planned and well documented.

The Three Stages Of The Statutory Residence Test

SRT works in three layers:

1. Automatic Overseas Tests

If you meet one of these, you are treated as non-resident.

2. Automatic Uk Tests

If you meet one of these, you are treated as UK resident.

3. Sufficient Ties Test

If neither automatic category applies, your residency depends on a combination of:

- Your UK ties

- Your UK day count in the tax year

- whether you are a “leaver” (UK resident in one or more of the previous three tax years) or an “arriver” (not UK resident in any of the previous three tax years)

- and, for leavers, whether the country tie applies (i.e., whether the UK is the single country where you spent the greatest number of days)

This is where the detail matters most, because small changes in ties or day counts can change the outcome.

Let’s break it down properly, in practical terms, not in jargon.

Automatic Overseas Tests (The Clearest Route To Non-Residence)

If you meet any of the following tests, you are treated as non-resident for that tax year.

Overseas Test 1 - The 16-Day Rule

You are non-resident if:

- You spent fewer than 16 days in the UK, and

- You were UK resident in any of the previous 3 tax years.

This is rarely relevant for most expats but can apply where UK presence is extremely limited.

Overseas Test 2 - The 46-Day Rule

You are non-resident if:

- You spent fewer than 46 days in the UK, and

- You were not UK resident in any of the previous 3 years.

This is most commonly relevant for long-term expats returning occasionally.

Overseas Test 3 - Full-Time Work Abroad Test

You are non-resident if all of the following apply:

- You work full time overseas under the “sufficient hours” test (broadly an average of 35 hours per week over the tax year, calculated using specific rules)

- You work fewer than 31 days in the UK (where a UK “workday” is generally a day with more than three hours of work in the UK)

- You spend fewer than 91 days in the UK

- There is no significant break in overseas work

Common reasons people unexpectedly fail this test include**:**

- Counting travel days incorrectly

- Working while in the UK without realising

- Not documenting work patterns

- “Shadow working” for UK entities

- Doing Zoom calls from the UK

- Taking one consulting day onshore

- Not tracking hours properly

Automatic UK Tests (Conditions You Should Manage)

If ANY of these apply, you are treated as UK resident, even if you live abroad.

Automatic UK Test 1 - The 183-Day Rule

If you spend 183 days or more in the UK, you are UK resident for that tax year.

Simple and clear in principle.

Automatic UK Test 2 - The UK Home Test

You are automatically resident if:

- You have a UK home available for at least one period of 91 consecutive days, and

- You spend 30+ days in that home, and

- You have no overseas home, or if you do, you spend fewer than 30 days in any overseas home in the tax year.

This is the test that often undermines the residency claims of:

- Expats whose spouse stays in the UK

- Expats who keep their UK home “just in case”

- Expats who Airbnb their home (still “available”)

- Expats who use the property occasionally

If someone else lives in your UK home, it can STILL be considered “available”.

This is a common reason residency outcomes differ from expectation.

Automatic UK Test 3 - The Full-Time Work in the UK

You are UK resident if you work sufficient hours in the UK over a 365-day period and at least one day of that period falls in the tax year, with no significant breaks from UK work and:

- more than 75% of the days in that 365-day period on which you do more than 3 hours’ work are days on which you do more than 3 hours’ work in the UK, and

- there is at least one UK workday (more than 3 hours’ work in the UK) that falls both within the 365-day period and within the relevant tax year.

This test is less common for people leaving the UK, but it can matter where someone returns and starts working in the UK mid-year.

{{INSET-CTA-1}}

The Sufficient Ties Test

If you do NOT meet an automatic overseas or UK test, your residency depends on your:

- UK ties

- day counts

- your prior residency status (arriver vs leaver)

- and if you are a leaver, whether the country tie applies

This is the heart of SRT.

Many expats run into issues here because ties can accumulate quietly, and the day-count threshold depends on whether you are an arriver or a leaver.

There are five UK ties:

- Family tie

- Accommodation tie

- Work tie

- 90-day tie

- Country tie

How many days you're allowed in the UK depends on how many ties you have.

The more ties you have, the fewer days you can spend.

Let’s break them down simply.

The Five UK Ties

1. The Family Tie

You have a family tie if:

- Your spouse/partner is in the UK

- Your minor children live in the UK

This tie alone can weaken residency claims for:

- commuters

- trial relocators

- couples not moving together

- expats whose kids finish school in the UK

The family tie is the hardest tie to break emotionally - and often one of the most challenging tax-wise.

2. The Accommodation Tie

You have this tie if you have a place to live in the UK that is available to you for a continuous period of 91 days or more, and you stay there during the tax year - typically:

- at least one night (for a property that is not a close relative’s home), or

- 16 nights or more if it is a close relative’s home

“Available” is a key statutory concept. You can fail the test even if you don’t own the property.

3. The Work Tie

Triggered if you do 40+ UK workdays in a tax year.

A “workday” is ANY day where you do 3+ hours of work.

Zoom calls count.

Emails count.

Meetings count.

One careless month can materially change your residency position.

4. The 90-Day Tie (The Past-Behaviour Condition)

If you were in the UK for more than 90 days in any of the previous two tax years, you will generally have this tie.

Even if those visits were innocent:

- holidays

- family visits

- business travel

It still applies.

5. The Country Tie (An Overlooked Condition)

If you are a leaver, and the UK is the country where you spent the most days in the tax year, you can have the country tie.

You don’t need to spend many days. You just need to spend more days in the UK than anywhere else.

This catches:

- digital nomads

- European commuters

- people who rotate between multiple countries

- people with irregular travel patterns

- business-first relocators

This tie can potentially undermine residency claims.

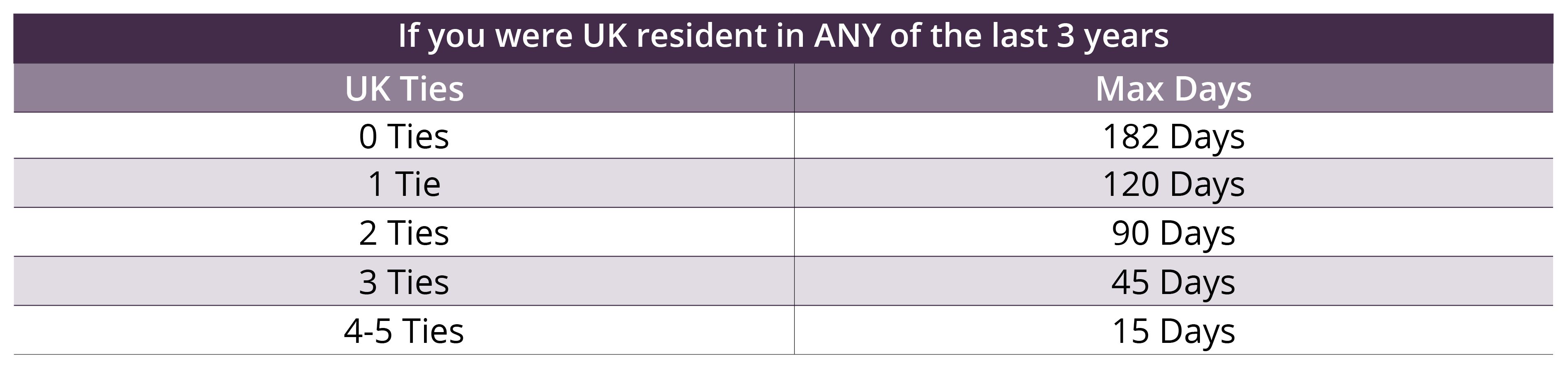

How Many Days Can You Spend In The Uk And Maintain Non-Uk Residence?

This is the part everyone gets wrong.

The number of ties you have determines how many days you can spend in the UK without becoming UK resident, and the thresholds differ depending on whether you are a leaver or an arriver.

If you were UK resident in ANY of the last 3 years:

If you were NOT resident in ANY of the last 3 years:

Many expats fall within the first table above because they are leavers (UK resident in one or more of the previous three tax years).

Meaning:

- 3 ties → only 45 days allowed

- 4 ties → only 15 days allowed

It can be easy to accumulate 3 ties without realising.

The New Reality (From 6 April 2025 And Beyond)

From 6 April 2025 onwards, residency matters even more because:

1. Non-dom regime abolished

Residency - not domicile - drives many UK tax outcomes.

2. A residence-based IHT test for long-term UK residents

Broadly, if you are UK resident for 10 of the previous 20 tax years, worldwide assets can fall within UK IHT, subject to detailed rules and potential ‘tail’ provisions on leaving.

3. Higher tax rates on investment-type income (phased)

Tax rate increases are phased: the ordinary and higher dividend rates rise from 6 April 2026 (the additional dividend rate remains unchanged), and savings and property income rates rise from 6 April 2027.” .

4. NI tightening

Becoming non-resident early helps plan your NI strategy.

5. HMRC scrutiny increased

Cross-border enforcement is rising.

{{INSET-CTA-2}}

Case Studies

Case Study 1 - The Commuting Consultant

Thought he lived in Dubai.

Worked 42 days in the UK.

Stayed at parents' house for 19 nights.

Had family tie + accommodation tie + work tie → 3 ties.

Spent 52 days in UK → resident.

Case Study 2 - The Family Problem

Father moved abroad.

Mother + kids stayed in Surrey.

Family tie and day counts resulted in UK residency.

Worldwide income taxed.

Case Study 3 – RSUs vesting

RSUs vested in a year she accidentally remained UK resident, resulting in a UK tax liability.

Case Study 4 - Mixed Travel Pattern

Spent 60 days in UK, 55 in UAE, 45 in Singapore, 40 in France.

UK = most days → country tie → residency triggered.

How To Actually Become Non-Resident

Step 1 - Set a clear departure date

Residency planning begins with intention + provable action.

Step 2 - Reduce ties BEFORE leaving

Remove:

- UK home availability

- frequent UK workdays

- unnecessary UK trips

- UK economic ties

Step 3 - Plan your day-count strategy for the ENTIRE tax year

Don’t just plan around your departure date.

Plan from 6 April to 5 April.

Step 4 - Manage your family tie

If your family stays in the UK, your days may become difficult to manage.

Step 5- Ensure your overseas work pattern is watertight

Document:

- hours

- contract

- travel

- visa

- residency proof

Step 6 - Remove “available accommodation” in the UK

This is the most misunderstood trap.

Step 7 - Avoid UK workdays

Emails, Zoom, calls, admin - all count.

Step 8 - Keep full records

HMRC enquiries often happen years later.

The Mistakes People Commonly Make

- Miscounting days

- Forgetting ties

- Returning too often

- Remote working from UK

- Leaving the UK mid-year

- Keeping a UK home “just in case”

- Letting RSUs vest in UK residence

- Not documenting intention

- Children staying in UK schools

- Using UK debit/credit cards frequently

- Not tracking spouses

- Relying on “common sense”

- Sleeping in a UK home more than 30 days

- Forgetting the country tie

- Failing the overseas work test due to poor evidence

What Happens If You Get SRT Wrong?

You become UK resident.

Meaning:

- UK tax can apply to worldwide income

- UK tax can apply to worldwide gains

- Overseas pension income may become taxable in the UK depending on the facts and any applicable treaty

- Overseas income and gains may need to be reported on your UK tax return (depending on your status and the nature of the income/gains)

- An IHT ‘tail’ can apply depending on long-term UK residence history

- NI issues appear

- Split-year denied

- HMRC can charge interest and penalties where returns are incorrect or tax is paid late (depending on the circumstances)

- double taxation issues can arise

The Non-Negotiable Truth About SRT

Residency isn’t emotional, and it isn’t determined by passports or how you feel you live. Under the SRT, it is driven by evidence: your UK days, work patterns, accommodation position and family connections. If the overall pattern of your life continues to point towards the UK, HMRC may still treat you as UK resident, even after a move abroad.

The Expat Checklist: How To Stay Non-Resident

- Track every UK day

- Track every UK workday

- Audit ties monthly

- Keep evidence

- Avoid UK home availability

- Avoid major UK life anchors

- Don’t allow UK to be “most days”

- Don’t commute back more than needed

- Move your centre of life - genuinely

Conclusion

Becoming non-resident isn’t complicated but it is precise.

If you understand the rules, prepare early and keep good evidence, you can often leave the UK cleanly and reduce the risk of tax complications following you.

If you rely on assumption - or advice from friends - or what you “think” residency is?

That’s when problems often arise.

With post-2025 changes and increased scrutiny, the stakes can feel higher than ever.

If you’re planning to become non-resident, it’s worth getting the SRT analysis right early. Fixing mistakes later is often difficult and expensive.

.jpeg)