Market Update

Q4 2025 Review & Q1 2026 Outlook

Skybound Group Chief Investment Strategist Jabir Sardharwalla reviews fund Commentary: Q4 2025 Review & Q1 2026 Outlook

January 30, 2026

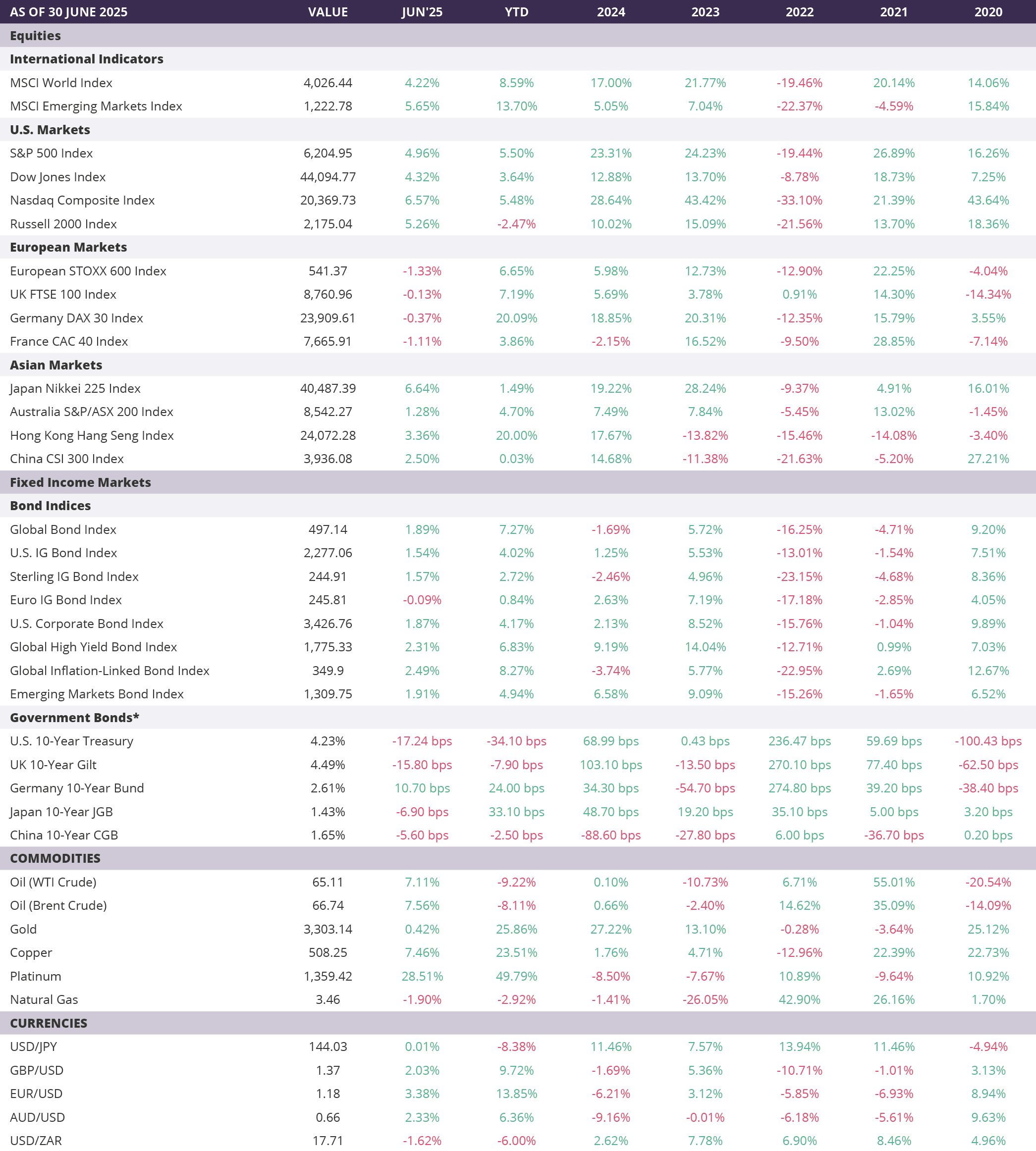

If you had been away since the start of the year without access to media and just returned, one look at the table below would suggest everything is fine. The YTD (Year-To-Date) performance numbers are impressive. Equities have been flying and, in a risk-on mode, Europe and EM has outperformed strongly. Germany and Hong Kong are standouts, both delivering in excess of 20% YTD.

However, those with access to media will know what scary times we have gone through in Q2! I am not going to dwell on the geopolitical situation other than to say things between Israel and Iran reached a key moment. For now, we have a cautious ceasefire in place and it seems to be holding. Throughout this, markets never sold off. Whether it comes down to complacency or just a genuine belief things would remain contained is hard to say. That aside, markets seem to be on a tear and, once again, tech seems to be rallying.

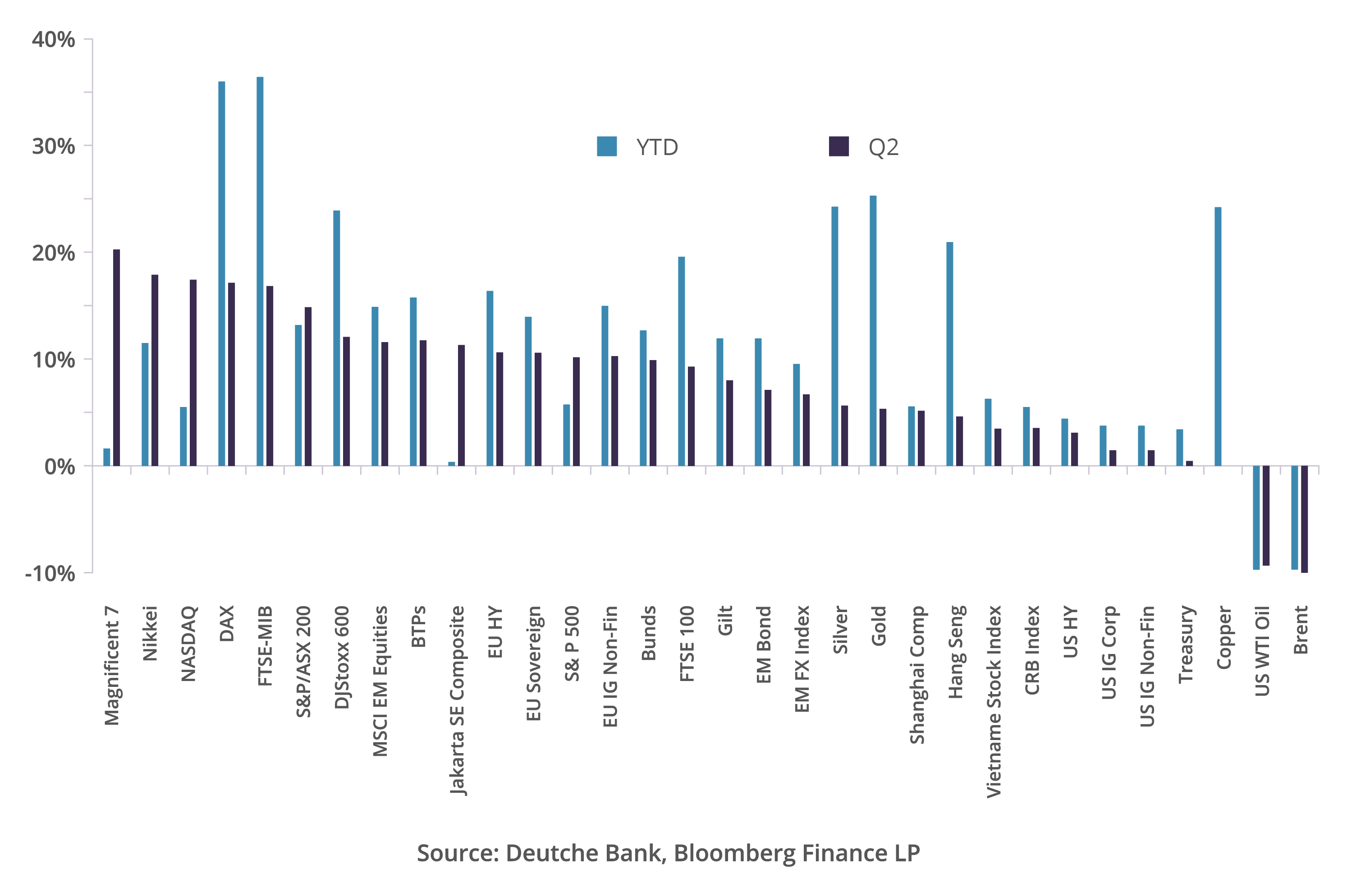

The second chart below (DB) is more discering. It splits performance over the recent quarter vs YTD for a select group of financial assets (expressed in US$ terms).

Certain things are striking:

FX: There is a definite US$ correction taking place as implied by the EM FX Index. Though not shown on there, the US$ Trade-Weighted Index conveys the same message.

Energy: After a brief spike during the height of the Israeli-Iranian conflict, oil prices very quickly collapsed back to their usual lows (mid-$60s). This will help reverse imminent inflationary concerns (primary and secondary).

Precious Metals: Gold, Silver, Copper, Platinum….are all flying! The latter two are very much a lack of inventory story while Gold is a central bank story particularly amongst certain Emerging Nations.

Countries/Regions: Germany, Spain, Italy,

China & Brazil are standout performers.

Sectors: Mag-7 had quite a comeback to finish positive YTD. If you missed that by being uninvested, then you took a big hit. The wider Nasdaq is a similar story.

Bonds: gained across the board to differing degrees.Like sectors, these gains were against a background of weakening US$ so, for non-US$ portfolios, the gains were even better in local FX terms.

Essentially, Q2 began with the historic sell-off immediately after the “Liberation Day announcement” on 2nd April. The S&P 500 fell over -10% marking its 5th biggest, two-day decline since WWII. Then came the 90-day announcement which sparked quite a bounce back. The US$ is down almost -11% YTD while sovereign bonds have shown good resilience with Italian 10y Bond (BTP) yields declining -26 bps (i.e. BTPs gained in value). Fiscal fears is the main worry (see Q3 Outlook section) and resulted in the long end, 30y Treasuries momentarily reaching 5.15% before falling below to 4.77%.

The following factors are going to define the outlook for Q3 and indeed the rest of the year and it will be largely driven by the US:

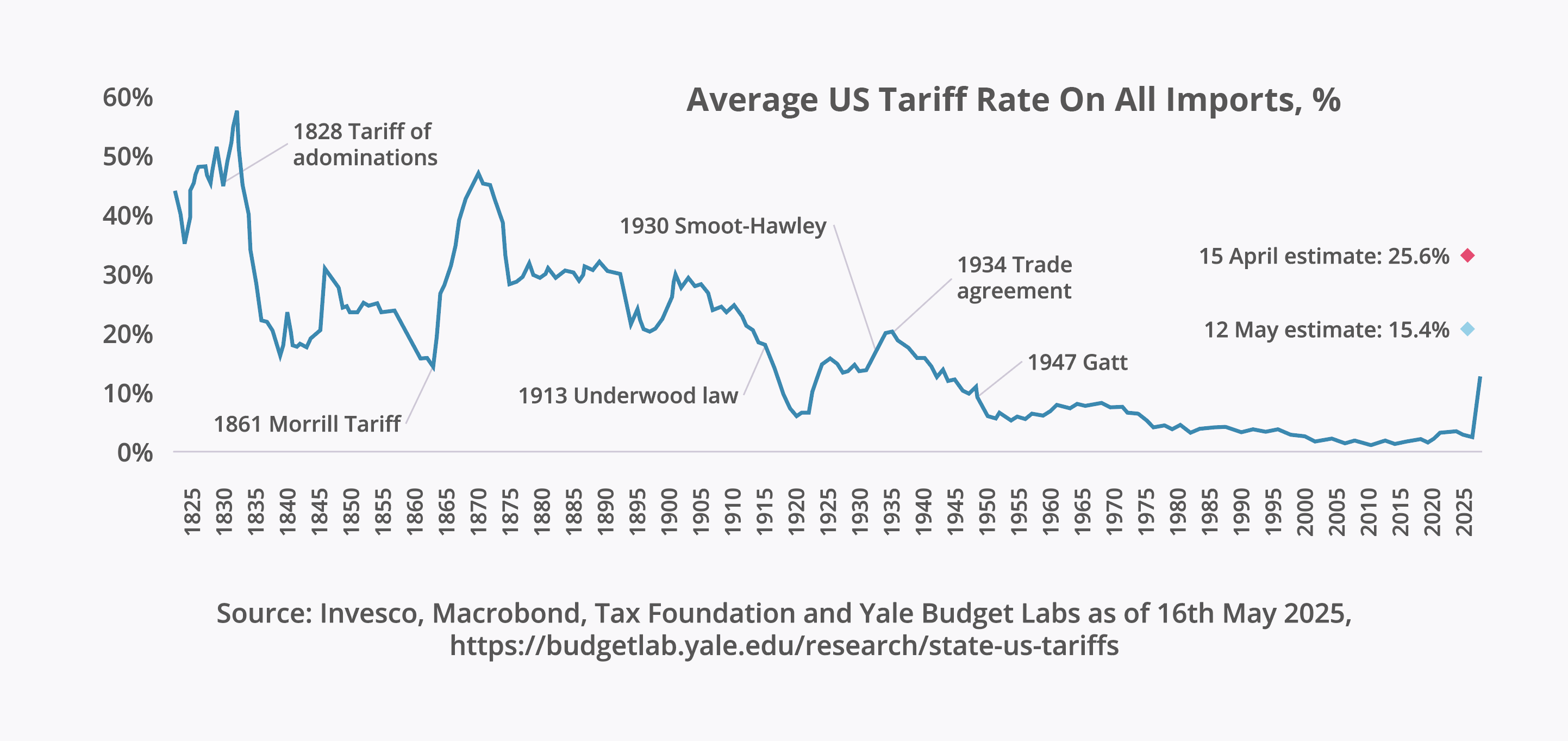

Tariffs

Based on negotiations so far, the effective tariff rate is around 15% mark (see chart below):

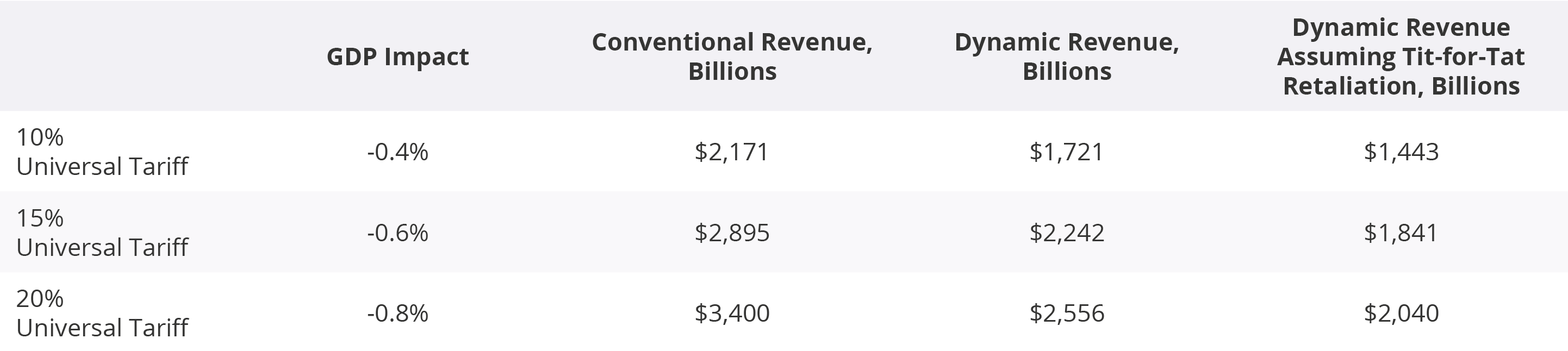

15% is probably not too far from where tariffs will eventually settle when all is concluded. A study conducted by the Tax Foundation concluded the estimated impact on US GDP would be as follows:

[Conventional = impact on revenue adjusted for changes in import behaviour (e.g. reduced volumes, substitution, etc). Dynamic = Conventional minus adjustments for revenue lost from an economic slowdown. Dynamic Tit-for-Tat = Dynamic minus adjustments for Tit-for-Tat behaviour.]

GDP is a poor story for other nations and regions: in real terms, the Euro-area is achieving half of its target, Japan is similar and China is under its top end range of 5% coming in at 4.3% to 4.7%.

Debt

US debt would be in the order of 125% to 130% of GDP – well above what is considered a good balance (90%). Critics argue above 90% implies a tipping point – the level of growth (GDP) needed starts to become too big a mountain to climb to then pay for that debt. By contrast, the Euro-area is just about on the mark (90%) vs its own target of 80% to 85%. The excess will come from Germany ramping up fiscal spending. Japan’s debt (mostly domestic) stands at around 255% of GDP (vs a target of 200%) while China’s is officially 84%.

Debt Servicing Costs

Currently, over 3% of US GDP is required just to pay for interest servicing! Contrast that with the Euro-area (2%), Japan (3%) and China (3%). The debt-servicing side of these major economies is the problem child.

CONCLUSION:

Debt burdens of prior years were not an issue because we lived through a decade of easy money (QE = Quantitative Easing). The result was non-existent/negative rates, ultra-low inflation and high growth. That’s all changing – money is no longer easy and comes with a cost (an opportunity cost). The debt-servicing costs are enough to fund a major department – at least boost several existing ones. The hurdle is rising and at some point, the athlete will trip over that hurdle because he/she cannot run any faster or jump any higher!

How can it be fixed?

For developed nations, it has to be from reducing costs and improving productivity and this will be a function of technology. We are already seeing it in application in many areas – healthcare, defence, agriculture and industry are some top examples. The benefit to GDP growth will be limited in matured markets – that’s the reason they are called Developed Markets!

What are the key risks we face?

Resurgent inflation (trade-driven supply shocks PLUS fiscal loosening) and deep recession (if business sentiment sinks and they start cutting back). The other risk is a Goldilocks scenario (led by an AI-productivity surge PLUS easing global tensions, both of which reignite inflation).

US: growth is slowing but no signs it is collapsing. The supply-side will come under pressure given the clampdown on migrants while the OBBB (One Big Beautiful Bill) will provide a big fiscal splurge. Together, these are inflationary.

Europe: Germany’s fiscal bazooka will be a boost and, given its better valuation metrics vs the US, will be attractive. Its innovation also should not be underestimated.

China: there are signs of property market stabilisation while it is developing its own exceptionalism driven by technology (especially AI and Robots). Together, this will be a much-needed confidence boost for its domestic economy.

Stay up-to-date with financial news and insights delivered straight to your inbox. Sign up today.