Skybound Wealth Management

Tax, Pensions & Long-Term Wealth Planning

Get Clarity. Take Control.

Contractors, Freelancers, and Business Owners Deserve Advice That Reflects Their Reality.

Variable income, IR35 considerations, complex remuneration structures, and significant assets that straddle personal and commercial lines - these aren't edge cases for Broadbench clients. They're the norm.

Arun Sahota is a UK-regulated Private Wealth Partner at Skybound Wealth, working with high-net-worth individuals, business owners, and senior professionals whose financial decisions carry long-term consequences. He advises across pensions, inheritance tax, investment structuring, and long-term wealth planning - integrating everything into a single, coherent strategy rather than treating each area in isolation.

Whether you're inside or outside IR35, Arun helps you structure your remuneration and long-term savings in a way that's tax-efficient, compliant, and built to last - not just optimised for this tax year.

From SIPPs and SSAS planning to long-term cashflow modelling, Arun builds retirement strategies around what you actually want your future to look like - not a generic projection.

Business owners and self-employed professionals often hold significant assets with real IHT exposure. Arun works through the structures, timing, and tools available to protect what you've built for the people who matter.

Business owners and self-employed professionals often hold significant assets with real IHT exposure. Arun works through the structures, timing, and tools available to protect what you've built for the people who matter.

Life cover, income protection, and policies written in trust - Arun ensures the protection side of your plan is as considered as the wealth-building side.

Start with a focused conversation where you share your income structure, assets, and the questions you haven't had straight answers to yet. Arun gets the full picture before any recommendations are made.

Arun maps your position across tax, pensions, investments, and protection - identifying where decisions in one area may be creating avoidable consequences in another, and where real opportunities exist.

Together you settle on a long-term strategy. No product-led recommendations, no bias toward platforms or providers - just independent, whole-of-market advice built around your objectives.

Arun's guidance is supported by Skybound Wealth's global infrastructure - deep cross-border expertise, award-winning advisory standards, and the tools to support clients with significant and complex financial positions.

6,000+ international clients & growing$1.5 Billion of client savings under management32 Industry Awards & Counting Since 202111 offices on 4 continents & more opening soon.

If you've got questions about how this works for someone in your position, you're not alone. These are the ones Arun gets asked most.

Quarterly reviews, ongoing rebalancing, regular portfolio factsheets — we’re with you for the long haul, adjusting your plan as life evolves.

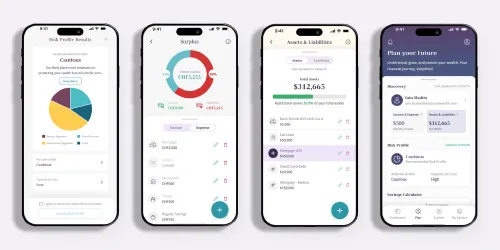

Manage your investments 24/7 with the Skybound Wealth App offering real-time portfolio views, performance summaries, and seamless adviser access.

Our exclusive SOAR magazine delivers cutting-edge insights, market updates, and strategies, keeping you informed, inspired, and in control.